Politicians often promise tax cuts can lead to higher productivity, higher economic growth, and even pay for themselves through a boost to long-term incomes. These promises may chime with the electorate who tend to prefer promises of tax cuts. But, do tax cuts really increase economic growth?

There are two impacts of lower tax.

Lower income tax rates increase the spending power of consumers and can increase aggregate demand, leading to higher economic growth (and possibly inflation).

On the supply side, income tax cuts may also increase incentives to work – leading to higher productivity.

However, the effect of tax cuts depends on how the tax cut is financed, the state of the economy and whether low tax rates actually increase productivity and the willingness to work.

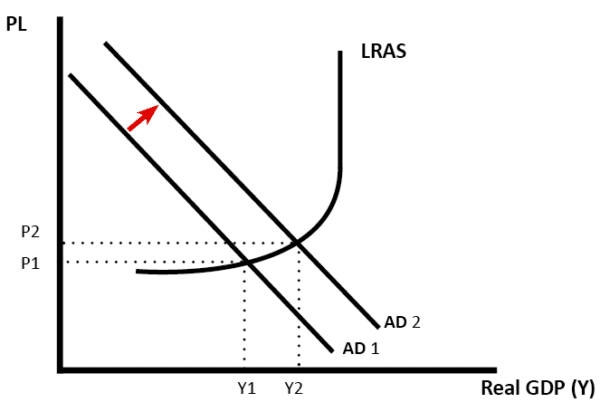

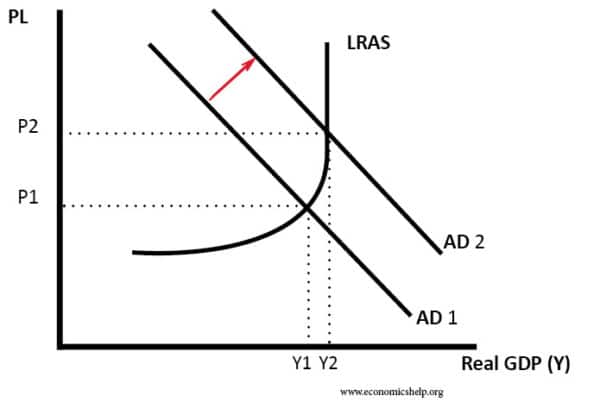

Effect of tax cut when the economy is below full capacity

Impact of tax cuts on AD/AS diagram, when there is spare capacity in the economy.

Will a cut in tax really increase aggregate demand? Firstly, it depends on how the tax cut is financed.

Cutting taxes when the economy is already growing quickly is likely to cause inflationary pressures.

In 1988, chancellor Nigel Lawson cut income tax. The top rate of tax was cut from 60p to 40p and the basic rate from 27p to 25p. These tax cuts occurred during a period of strong economic growth; these tax cuts (combined with loose monetary policy) led to even higher economic growth, but inflation also increased to 8% in 1989 and caused a subsequent boom and bust. The tax cuts also caused a rise in import spending and an increase in the UK current account deficit.

If we take a cut in income tax, it could also affect the supply side of the economy.

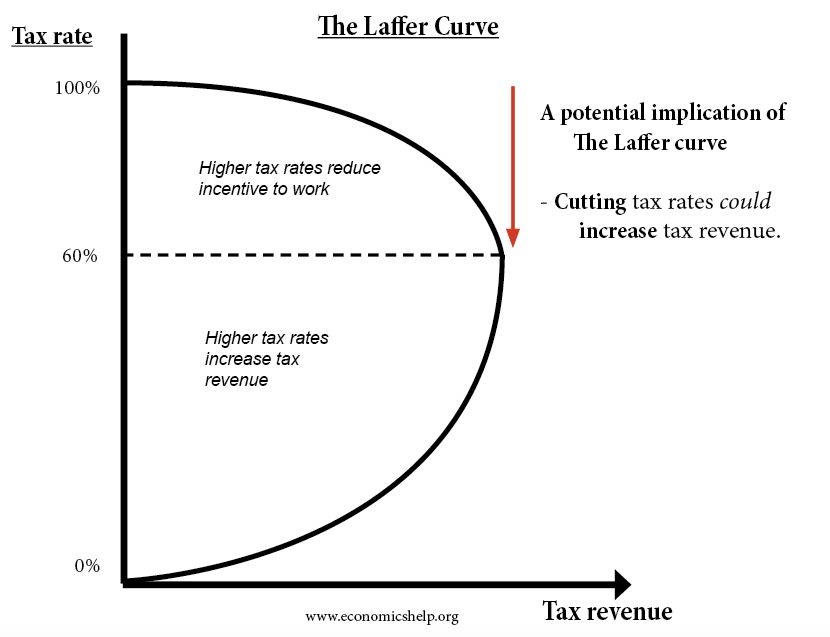

A controversial economic argument is the “Laffer Curve“. This argues that if you cut income tax rates, then the tax cut increases the incentive to work so much, that the government can actually gain more tax revenue. It seems to offer the best of both worlds – lower tax rates and higher tax revenues.

There is a debate about the extent to which tax cuts increase productivity and economic growth. If marginal income tax rates are very high, e.g. 80%, then cutting tax rates is likely to increase labour supply and productivity. But, with tax rates of 20 or 30%, cutting income tax rates is no guarantee of increasing productivity and growth.

If the government cut an indirect tax like VAT, the effect is similar. If goods are cheaper because of lower tax, consumers will effectively have more purchasing power. After buying the same number of goods, they will have more money left over. Therefore consumer spending may rise. There will be little impact on productivity.

Short-term. If the economy is close to full employment with a low saving ratio, then tax cuts financed by borrowing from the private sector could well ‘crowd out‘ the extra disposable income consumers have. Therefore, the impact on growth is limited, but it will cause higher inflation.

However, in a recession, when saving rates are very high, then government borrowing doesn’t remove money from the economy because it was just been saved.

Ricardian Equivalence

Another issue is the idea that consumers may respond to tax cuts by deciding to save more. The reason is that rational consumers may see a tax cut financed by borrowing will lead to future tax rises. Therefore, consumers don’t spend the tax cut but save it for future tax rises. More on: Ricardian equivalence

1. The Economic Consequences of Major Tax Cuts for the Rich, by David Hope and Julian Limberg, found tax cuts for the rich, had no statistical effect on economic growth

“The results also show that economic performance, as measured by real GDP per capita and the unemployment rate, is not significantly affected by major tax cuts for the rich. The estimated effects for these variables are statistically indistinguishable from zero.” (LSE)

2. Do corporate tax cuts boost economic growth? European Economic Review

Volume 147, August 2022, 104157. This study found that some studies suggest a 10% cut in corporation tax leads to 2% rise in GDP. But, they found “publication selectivity in favour of reporting growth-enhancing effects of corporate tax cuts.” Adjusting for bias, they conclude:

“Our finding that the average effect of corporate tax cuts on growth is zero with some variance for individual cases.”

3. NBER June 1997 Engen and Skinner conclude that

“cutting marginal tax rates across the board by 5 percentage points and cutting average tax rates by 2.5 percentage points would increase the growth rate of U.S. GDP by 0.3 percentage points per year.”

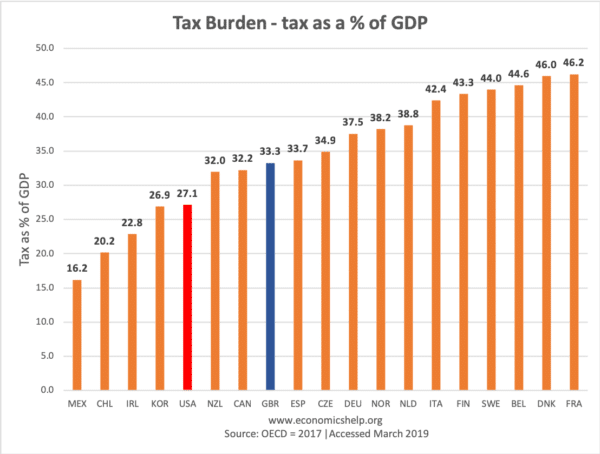

It is hard to spot a correlation between the tax burden and wealth. France and Denmark have a tax burden of 46% of GDP and a similar GDP per capita to the USA which has a tax burden of only 27%

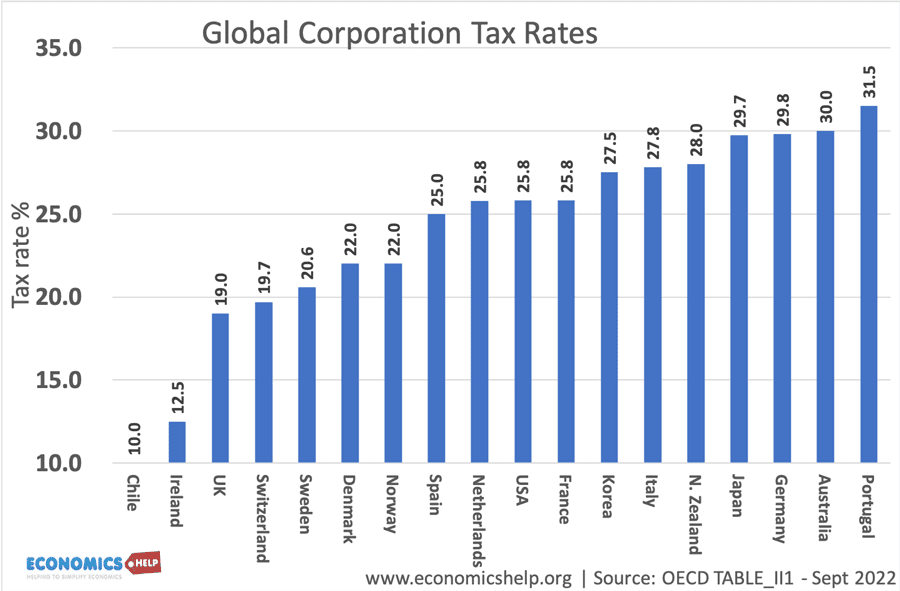

Global Corporation taxes

It is a similar story with global corporation tax rates. varying from 31% in Denmark to 12% in Ireland. The US corporation tax rate was reduced to 21% shortly after this graph.

Related